Hyperparameters Tuning for XGBoost using Bayesian Optimization

A non-technical yet detailed guide to implement hyperparameter tuning for XGBoost

credit: unsplash

credit: unsplash

TL;DR

I covered a brief introduction to XGBoost in the SMU Master of Professional Accounting program' elective course Programming with Data. This post is to provide an example to explain how to tune the hyperparameters of package:xgboost using the Bayesian optimization as developed in the ParBayesianOptimization package. I also demonstrate how parallel computing can save your time and computing resources.

Hyperparameter vs. parameter

I will start with a package:xgboost model with default hyperparameter values.

What? What is hyperparameter?

You must have heard about parameters such as \(\alpha\) and \(\beta\) in the ordinary least square (OLS) and Logistic regression models. So what is hyperparameter and what is the difference from parameter?

hyperparameter: a parameter which needs to be specified before we train the model, such aslamdain the LASSO model andlearing ratein the XGBoost model. These parameters will be used to control the machine learning process.parameter: the coefficient/weight to be derived from machines learning process, such as\(\alpha\)and\(\beta\)in the OLS regression

Did you notice that we don’t have to specify any hyperparameter when we employ the OLS and the normal Logistic models as they don’t have any hyperparameters. However, for more complex machine learning models such as LASSO, Random Forest and XGBoost, we need to specify some hyperparameters before we run the models.

For XGBoost, all the hyperparameters are available here. You may note that all those hyperparametes have default values which come with the XGBoost package. It means that if you don’t specify any new values, the model will use the default values to control the training process. If you want to change the values of hyperparameters, you need to specify them before training the model. This process is called hyperparameter tuning in the machine learning lingo.

Then why do we need to tune the hyperparameters? A simple and intuitive answer is to fine tune your model which can better train your model and hence produce better results. When you buy your mobile phone, you’d like to choose color, size and capacity. It is the same logic when you try to run complex machine learning models. So one configuration does not fit all.

XGBoost with default hypterparameter values

We will use the following packages: package:xgboost and package:ParBayesianOptimization. Both are available on the CRAN package depository which can be installed directly from RStudio or the install.packages() function.

library(xgboost)

library(ROCR)

library(ggplot2)

library(ParBayesianOptimization)

The data I will be using is a proprietary dataset of class action lawsuit. Our objective is to predict the class action lawsuit binary outcome which takes value of 1 for a class action lawsuit and 0 for none. It is labeled as legal in the dataset. So this is a typical binary classification problem. The features include companies' financial information and non-financial information such as the readability of annual report.

As I mentioned in class, if your data is large, you should use the fread() which is much faster than the read.csv(). You need to install package:data.table before running the following code.

training <- data.table::fread("training.csv")

testing <- data.table::fread("testing.csv")

Let’s first define the formula as follows. As my focus of this post is not to explain the data, I will skip data exploration. You would be able to guess what each feature means from its name.

# Equation for the regression. -1 removes the intercept

eq = as.formula("legal ~ adj_return_FY + volume_FY + std_ret_FY +

skew_ret_FY + log_size + growth + fps +

Coleman_Liau_Index + Gunning_Fog_Index +

averageWordsPerSentence + WordCount +

FinTerms_Negative + FinTerms_Positive +

FinTerms_Litigious + FinTerms_Uncertainty - 1")

Next, we need to prepare the x data (predictors) and the y data (prediction or label) which meet the format requirement for package:xgboost. XGBoost also has its own data format using xgb.DMatrix() which I will use later.

# Make matrices for training data

x <- model.matrix(eq, data = training)

y <- model.frame(eq, data = training)[ , "legal"]

# Make matrices for testing data

xvals <- model.matrix(eq, data = testing)

yvals <- model.frame(eq, data = testing)[ , "legal"]

Now we are ready to try the XGBoost model with default hyperparameter values. We look at the following six most important XGBoost hyperparameters:

max_depth[default=6]: Maximum depth of a tree. Increasing this value will make the model more complex and more likely to overfit. Range: [0,∞]eta[default=0.3]: The learning rate. Range: [0,1]gamma[default=0]: Minimum loss reduction required to make a further partition on a leaf node of the tree. The larger gamma is, the more conservative the algorithm will be. Range: [0,∞]min_child_weight[default=1]: Minimum number of observations needed in a child node. The larger min_child_weight is, the more conservative the algorithm will be. Range: [0,∞]subsample[default=1]: Subsample ratio of the training instances (observations). Setting it to 0.5 means that XGBoost would randomly sample half of the training data prior to growing trees. The default is 1 which means no subsample process. Subsampling will occur once in every boosting iteration. It is used to minimize the overfitting problem. Range: (0,1]nfold: number of cross validation (CV) folds. There is no default value and we start with the typical 10 folds cross validation. We will tune it with the range of 3 to 10 later. As this is for CV only, I will define it in thexgb.cv()function.

In addition to the above six parameters, we also specify the following hyperparameters:

booster[default=gbtree]: tree-based boosting method. This can be used for both classification and regression problems.objective[default=reg:squarederror]: loss function, the default is for OLS. We will usebinary:logisticfor binary classificationeval_metric[default according to objective]: Evaluation metrics for validation data, a default metric will be assigned according to objective (rmsefor regression, andloglossfor classification,mean average precisionfor ranking). We will useaucfor binary classificationverbosity[default=1]: printing messages while training the model, 0 (silent, ie,not showing any message), 1 (warning), 2 (info), 3 (debug)

The following code specifies the default value for each hyperparameter. We will try to tune these hyperparameters later.

set.seed(2021)

# The first five params to be tuned are set to default values

params <- list(max_depth = 6,

eta = 0.3,

gamma = 0,

min_child_weight = 1,

subsample = 1,

booster = "gbtree",

objective = "binary:logistic",

eval_metric = "auc",

verbosity = 0)

To minimize the overfitting problem, we use the cross validation (CV) function xgb.cv()

to find out the best number of rounds (boosting iterations) for XGBoost. We use 10-fold cross validation for 100 rounds with evaluation matrix of AUC. The optimal number of rounds is determined by the minimum number of rounds which can produce the highest validation AUC (ie, lowest validation error).

The following are additional parameters for xgb.cv():

nrounds: the max number of boosting iterationsprediction: return the test fold predictions from each CV modelshowsd: show standard deviation of cross validationearly_stopping_rounds: CV will stop if the performance not improve for the specified roundsmaximize: maximize the performance forearly_stopping_roundsstratified: a boolean indicating whether sampling of folds should be stratified by the values of outcome labels (ie, the same distribution).

xgbCV <- xgb.cv(params = params,

data = x,

label = y,

nrounds = 100,

prediction = TRUE,

showsd = TRUE,

early_stopping_rounds = 10,

maximize = TRUE,

nfold = 10,

stratified = TRUE)

## [1] train-auc:0.608586+0.055258 test-auc:0.572297+0.068084

## Multiple eval metrics are present. Will use test_auc for early stopping.

## Will train until test_auc hasn't improved in 10 rounds.

##

## [2] train-auc:0.678191+0.033688 test-auc:0.650105+0.079131

## [3] train-auc:0.719241+0.006678 test-auc:0.698039+0.059299

## [4] train-auc:0.759246+0.042095 test-auc:0.719033+0.051714

## [5] train-auc:0.790659+0.025629 test-auc:0.754845+0.058458

## [6] train-auc:0.813285+0.019499 test-auc:0.763808+0.066096

## [7] train-auc:0.833346+0.023242 test-auc:0.774066+0.069199

## [8] train-auc:0.854651+0.020619 test-auc:0.779899+0.071212

## [9] train-auc:0.872086+0.020359 test-auc:0.783353+0.057533

## [10] train-auc:0.899344+0.005392 test-auc:0.805547+0.051509

## [11] train-auc:0.912967+0.005048 test-auc:0.806929+0.043305

## [12] train-auc:0.920942+0.005632 test-auc:0.808565+0.042629

## [13] train-auc:0.935232+0.009637 test-auc:0.808077+0.052455

## [14] train-auc:0.954605+0.006817 test-auc:0.795913+0.054406

## [15] train-auc:0.965291+0.004774 test-auc:0.799948+0.046381

## [16] train-auc:0.976118+0.005211 test-auc:0.795866+0.039994

## [17] train-auc:0.981229+0.004516 test-auc:0.791373+0.037651

## [18] train-auc:0.985593+0.003656 test-auc:0.805069+0.042414

## [19] train-auc:0.988762+0.002436 test-auc:0.807052+0.043763

## [20] train-auc:0.991113+0.002288 test-auc:0.804686+0.049946

## [21] train-auc:0.992633+0.001731 test-auc:0.809471+0.047058

## [22] train-auc:0.994259+0.001353 test-auc:0.805859+0.045883

## [23] train-auc:0.995357+0.001078 test-auc:0.806442+0.046140

## [24] train-auc:0.996342+0.000797 test-auc:0.800382+0.046470

## [25] train-auc:0.997282+0.000579 test-auc:0.802973+0.049742

## [26] train-auc:0.997959+0.000565 test-auc:0.802661+0.053013

## [27] train-auc:0.998488+0.000446 test-auc:0.798695+0.055943

## [28] train-auc:0.998864+0.000299 test-auc:0.797324+0.057295

## [29] train-auc:0.999128+0.000299 test-auc:0.794634+0.059362

## [30] train-auc:0.999378+0.000281 test-auc:0.793525+0.061460

## [31] train-auc:0.999553+0.000221 test-auc:0.789565+0.061613

## Stopping. Best iteration:

## [21] train-auc:0.992633+0.001731 test-auc:0.809471+0.047058

numrounds <- min(which(xgbCV$evaluation_log$test_auc_mean ==

max(xgbCV$evaluation_log$test_auc_mean)))

Finally, we can fit the XGBoost model as follows.

fit <- xgboost(params = params,

data = x,

label = y,

nrounds = numrounds)

## [1] train-auc:0.649467

## [2] train-auc:0.718068

## [3] train-auc:0.718619

## [4] train-auc:0.796286

## [5] train-auc:0.797473

## [6] train-auc:0.861141

## [7] train-auc:0.861677

## [8] train-auc:0.867764

## [9] train-auc:0.880949

## [10] train-auc:0.892904

## [11] train-auc:0.903122

## [12] train-auc:0.915757

## [13] train-auc:0.921750

## [14] train-auc:0.931584

## [15] train-auc:0.953188

## [16] train-auc:0.964687

## [17] train-auc:0.975628

## [18] train-auc:0.980401

## [19] train-auc:0.982171

## [20] train-auc:0.984214

## [21] train-auc:0.988682

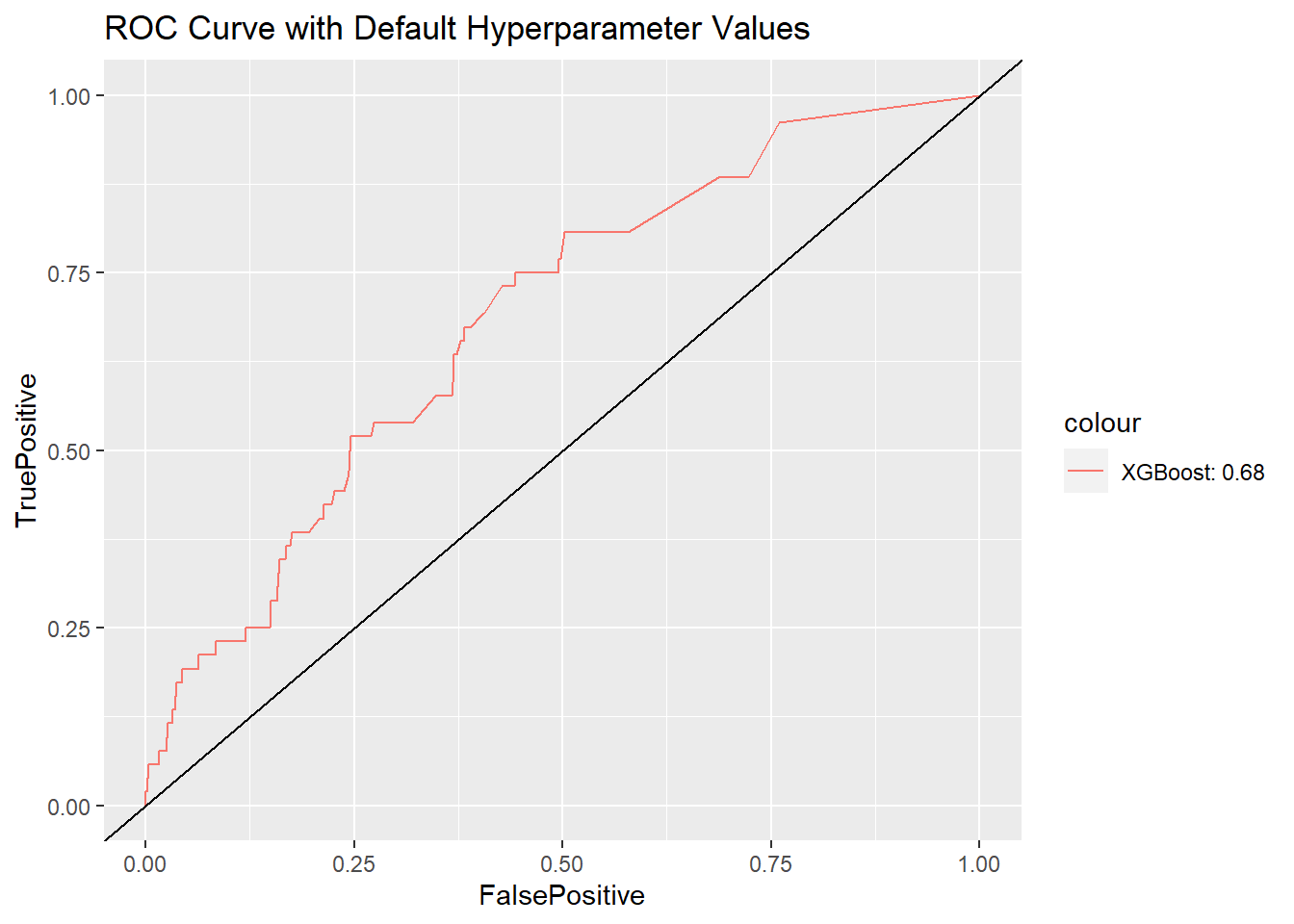

How does this model work for the testing data? Let’s compute the AUC using the package:ROCR. The value of AUC using default hyperparameter values is 0.68, which is not bad.

pred.xgb <- predict(fit, xvals, type = "response")

ROCpred.xgb <- prediction(as.numeric(pred.xgb), as.numeric(yvals))

auc.xgb <- performance(ROCpred.xgb, measure = "auc")

auc <- auc.xgb@y.values[[1]]

names(auc) <- c("XGBoost AUC")

auc

## XGBoost AUC

## 0.6836743

We can also plot the curve.

ROCperf.xgb <- performance(ROCpred.xgb, 'tpr','fpr')

df_ROC.xgb <- data.frame(FalsePositive = c(ROCperf.xgb@x.values[[1]]),

TruePositive = c(ROCperf.xgb@y.values[[1]]))

ggplot() +

geom_line(data = df_ROC.xgb, aes(x = FalsePositive,

y = TruePositive,

color = "XGBoost: 0.68")) +

geom_abline(slope = 1) +

ggtitle("ROC Curve with Default Hyperparameter Values")

Hyperparameter tuning with bayesian optimization

The above model uses all default values of hyperparameters and the AUC is 0.68. The next question is: can we change the parameter values and achieve better results? Intuitively, we can manually try different values using for loops and compare the results (pick the one with lowest validation error) like this post. There is also packages which can help to automate this grid search process such as the package:MLR.

This process is in fact an optimization problem: minimize the validation errors. Instead of manual grid search, We can use optimization algorithm to search for the best parameter values. This is what the package:ParBayesianOptimization is trying to do.

Let me walk you through the optimization process. Please note that I typically don’t use capital letters for variable names but the package:ParBayesianOptimization defines a lot of objects using capital letters.

Define an optimizing function

This optimization function will take the tuning parameters as input and will return the best cross validation results (ie, the highest AUC score for this case). The package:ParBayesianOptimization uses the Bayesian Optimization.

In the following code, I use the XGBoost data format function xgb.DMatrix() to prepare the data.

scoring_function <- function(

eta, gamma, max_depth, min_child_weight, subsample, nfold) {

dtrain <- xgb.DMatrix(x, label = y, missing = NA)

pars <- list(

eta = eta,

gamma = gamma,

max_depth = max_depth,

min_child_weight = min_child_weight,

subsample = subsample,

booster = "gbtree",

objective = "binary:logistic",

eval_metric = "auc",

verbosity = 0

)

xgbcv <- xgb.cv(

params = pars,

data = dtrain,

nfold = nfold,

nrounds = 100,

prediction = TRUE,

showsd = TRUE,

early_stopping_rounds = 10,

maximize = TRUE,

stratified = TRUE

)

# required by the package, the output must be a list

# with at least one element of "Score", the measure to optimize

# Score must start with capital S

# For this case, we also report the best num of iteration

return(

list(

Score = max(xgbcv$evaluation_log$test_auc_mean),

nrounds = xgbcv$best_iteration

)

)

}

Set the boudary for each tuning parameter

Next we will define the boundary of values for each tuning parameter. Note that we need to specify integer if it takes integer values only, including max_depth and nfold. You may try different boundary but all must be in the range of values which are permitted by the parameters.

# define the lower and upper bounds for each function (FUN) input

bounds <- list(

eta = c(0, 1),

gamma =c(0, 100),

max_depth = c(2L, 10L), # L means integers

min_child_weight = c(1, 25),

subsample = c(0.25, 1),

nfold = c(3L, 10L)

)

Start the optimization process

The optimization process is handled by the bayesOpt() function which will maximize the optimization function using Bayesian optimization.

FUNis the defined function for optimizationboundsis the boundary of values for all parametersinitPoints: initialized the optimization process by running FUN number of times, the value must be more than the number of FUN inputs (for this case, FUN has 6 inputs, so this value should be at least 7). Intuitively this is to create some initial data points for subsequent optimization process and hence the number of data points should be more than the number of unknown variables in the FUN function (remember degree of freedom for a linear regression?). This process is also to form the prior belief for Bayesian statistics.iters.n: times FUN to run after initialization to search for global optimal solutions. It is to update prior belief and form posterior belief. So the following will have 7+5=12 times of run of FUN. You can set a different value and a higher value will demand more computing power and time.

The following code will take a while, so have a break. To see how long it takes, I use the system.time() to record the time consumed by running the function. This is also to compare with parallel computing I am going to explain later.

set.seed(2021)

time_noparallel <- system.time(

opt_obj <- bayesOpt(

FUN = scoring_function,

bounds = bounds,

initPoints = 7,

iters.n = 5,

))

The time spent is 193 seconds.

Let’s take a look at the output from the optimization process.

# again, have to use capital letters required by the package

# take a look at the output

opt_obj$scoreSummary

## Epoch Iteration eta gamma max_depth min_child_weight subsample

## 1: 0 1 0.3877129 5.830197 3 23.636865 0.6108428

## 2: 0 2 0.2212328 33.769044 9 18.423585 0.9221549

## 3: 0 3 0.1352906 28.441204 9 6.792980 0.4921414

## 4: 0 4 0.7216981 49.755068 6 17.583833 0.3108776

## 5: 0 5 0.9143621 89.247314 5 12.051483 0.3587631

## 6: 0 6 0.7045017 58.301765 3 3.197468 0.8747930

## 7: 0 7 0.4493588 77.719258 7 10.302494 0.7575065

## 8: 1 8 0.4264940 94.363057 2 4.927643 1.0000000

## 9: 2 9 0.4486033 0.000000 3 25.000000 1.0000000

## 10: 3 10 0.0000000 0.000000 3 25.000000 0.3191284

## 11: 4 11 0.4919245 0.000000 2 25.000000 0.2500000

## 12: 5 12 0.4216330 0.000000 2 3.650199 0.2500000

## nfold gpUtility acqOptimum inBounds Elapsed Score nrounds errorMessage

## 1: 9 NA FALSE TRUE 1.88 0.8251750 13 NA

## 2: 6 NA FALSE TRUE 0.75 0.5000000 1 NA

## 3: 8 NA FALSE TRUE 0.89 0.5000000 1 NA

## 4: 3 NA FALSE TRUE 0.25 0.5000000 1 NA

## 5: 5 NA FALSE TRUE 0.39 0.5000000 1 NA

## 6: 6 NA FALSE TRUE 0.92 0.6244403 7 NA

## 7: 7 NA FALSE TRUE 1.91 0.7156390 15 NA

## 8: 10 0.5194763 TRUE TRUE 2.23 0.7226113 22 NA

## 9: 3 0.4265991 TRUE TRUE 0.44 0.8273497 15 NA

## 10: 3 0.4780133 TRUE TRUE 0.18 0.5000000 1 NA

## 11: 8 0.4184995 TRUE TRUE 0.79 0.8240030 9 NA

## 12: 3 0.4124220 TRUE TRUE 0.50 0.7943757 20 NA

What we really want is the optimized values for the six parameters we want to tune. The getBestPars() function will report the values.

# the built-in function output the FUN input arguments only.

getBestPars(opt_obj)

## $eta

## [1] 0.4486033

##

## $gamma

## [1] 0

##

## $max_depth

## [1] 3

##

## $min_child_weight

## [1] 25

##

## $subsample

## [1] 1

##

## $nfold

## [1] 3

Train the tuned XGBoost model

We will take the optimized values for the six parameters and train the XGBoost model again. This supposes to create the highest AUC within the boundary values we set for the six parameters.

# take the optimal parameters for xgboost()

params <- list(eta = getBestPars(opt_obj)[1],

gamma = getBestPars(opt_obj)[2],

max_depth = getBestPars(opt_obj)[3],

min_child_weight = getBestPars(opt_obj)[4],

subsample = getBestPars(opt_obj)[5],

nfold = getBestPars(opt_obj)[6],

objective = "binary:logistic")

# the numrounds which gives the max Score (auc)

numrounds <- opt_obj$scoreSummary$nrounds[

which(opt_obj$scoreSummary$Score

== max(opt_obj$scoreSummary$Score))]

fit_tuned <- xgboost(params = params,

data = x,

label = y,

nrounds = numrounds,

eval_metric = "auc")

## [1] train-auc:0.560903

## [2] train-auc:0.649098

## [3] train-auc:0.790024

## [4] train-auc:0.793304

## [5] train-auc:0.854169

## [6] train-auc:0.858309

## [7] train-auc:0.864346

## [8] train-auc:0.868881

## [9] train-auc:0.872241

## [10] train-auc:0.881432

## [11] train-auc:0.882291

## [12] train-auc:0.885383

## [13] train-auc:0.893123

## [14] train-auc:0.891645

## [15] train-auc:0.892842

Evaluation of the tuned model

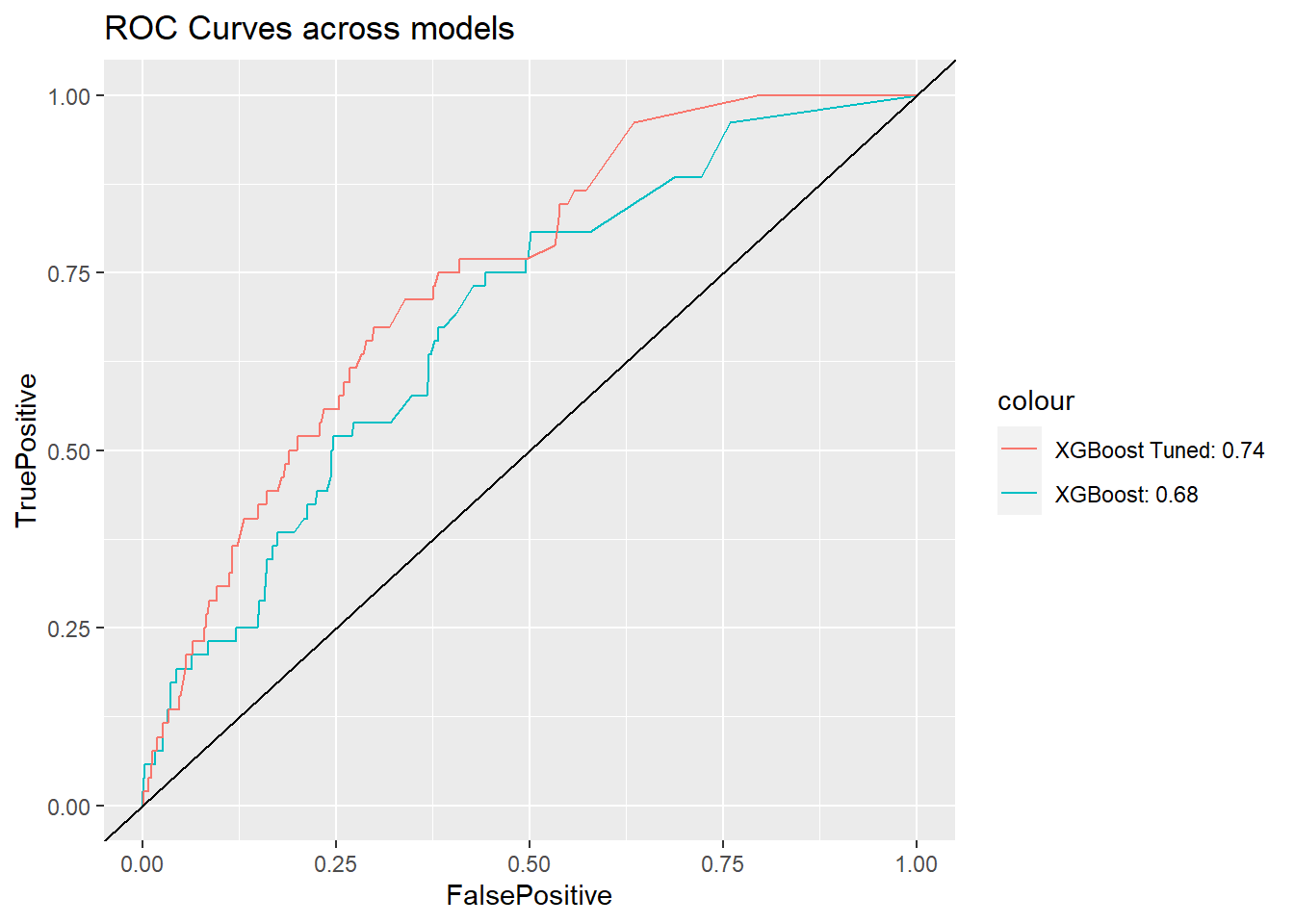

So how much is the AUC for the tuned model?

# Usual AUC calculation

pred.xgb.tuned <- predict(fit_tuned, xvals, type = "response")

ROCpred.xgb.tuned <- prediction(as.numeric(pred.xgb.tuned), as.numeric(yvals))

auc.xgb.tuned <- performance(ROCpred.xgb.tuned, measure = "auc")

auc <- auc.xgb.tuned@y.values[[1]]

names(auc) <- c("XGBoost AUC Tuned")

auc

## XGBoost AUC Tuned

## 0.7416419

The tuned model AUC is 0.7416419 which is much higher than the model with default paraeters. Yeah, we have improved the model by tuning the parameters.

Lastly, let’s plot the curves.

ROCperf.xgb.tuned <- performance(ROCpred.xgb.tuned, 'tpr','fpr')

df_ROC.xgb_tune <- data.frame(FalsePositive = c(ROCperf.xgb.tuned@x.values[[1]]),

TruePositive = c(ROCperf.xgb.tuned@y.values[[1]]))

ggplot() +

geom_line(data = df_ROC.xgb, aes(x = FalsePositive,

y = TruePositive,

color = "XGBoost: 0.68")) +

geom_line(data = df_ROC.xgb_tune, aes(x = FalsePositive,

y = TruePositive,

color = "XGBoost Tuned: 0.74")) +

geom_abline(slope = 1) + ggtitle("ROC Curves across models")

Bonus: Parallel computing

You may experience long waiting time when you try to train more complex machine learning models using larger data set. For the optimization process we tried above, it takes more than 3 minutes. But did you know that your computer can run the function simultaneously? Computer CPU has multiple threads/cores which can do parallel computing.

I will demonstrate how we can run parallel computing using the package:doParallel. The package:ParBayesianOptimization also supports parallel computing.

Don’t know how many cores/threads your CPU has? Don’t worry, we can use the detectCores() to find the number. Note that you’d better not use all of your cores to prevent crash of your computer. My computer has 6 cores and 12 threads and I am using half for this example (ie, 6 threads).

To enable the parallel computing, you must meet the following criteria:

- Make a socket cluster for multiple threads/cores working together. This is done by the

makeCluster()function. - A parallel backend must be registered, this is done by the

registerDoParallel()function. - Objects required by FUN must be loaded into each cluster. This will be done by the the

clusterExport()function. For our example, the FUN function needs to use the dataxandywhich are defined outside of the FUN function. - Packages required by FUN must be loaded into each cluster. This will be done by the the

clusterEvalQ()function. For our example, the FUN function needs thepackage:xgboostas it uses thexgb.DMatrix()function. - FUN must be thread safe. It means the function can be run simultaneously on multiple threads and the results should be the same as running on one thread serially. For example, each run of the FUN should be independent and one run of FUN is not depend on the previous run of FUN. You may refer more knowledge on thread safe coding here.

In addition, you must enable the parallel = TRUE option in the bayesOpt() function. After done with paralleing computing, you must stop it and continue with serial computing by using the stopCluster() and registerDoSEQ().

Okay, we are ready for the code.

set.seed(2021)

library(doParallel)

no_cores <- detectCores() / 2 # use half my CPU cores to avoid crash

cl <- makeCluster(no_cores) # make a cluster

registerDoParallel(cl) # register a parallel backend

clusterExport(cl, c('x','y')) # import objects outside

clusterEvalQ(cl,expr= { # launch library to be used in FUN

library(xgboost)

})

time_withparallel <- system.time(

opt_obj <- bayesOpt(

FUN = scoring_function,

bounds = bounds,

initPoints = 7,

iters.n = 5,

parallel = TRUE

))

stopCluster(cl) # stop the cluster

registerDoSEQ() # back to serial computing

The time spent is 52.19 seconds, which is much faster than without parallel computing (193 seconds).

Done!

Thanks for reading this post and I hope you find it useful. It is indeed a very fun process when you are able to get better results.

In sum, we start our model training using the XGBoost default hyperparameters. We then improve the model by tuning six important hyperparameters using the package:ParBayesianOptimization which implements a Bayesian Optimization algorithm. I also demonstrate the parallel computing which significantly saves computing time and resources.

Feel free to try hyperparameter tuning in your group project. Let me know if you have any questions by booking my time at https://calendly.com/drdataking.

This post is a supplementary reading to the SMU Master of Professional Accounting program' elective course Programming with Data.

Last updated on 07 November, 2021

Wang Jiwei

Associate Professor

My current research/teaching interests include digital transformation and data analytics in accounting.